Money Mistakes That Keep People Broke (And How to Avoid Them)

WhatsApp

Telegram

Facebook

Twitter

LinkedIn

Join Our WhatsApp Channel

Part 2A: Main Article (Sections 1–5)

Why Good Financial Habits Matter

Money isn’t just about how much you earn—it’s about how well you manage what you have. Many people believe a higher salary automatically leads to financial success, but that’s rarely true. Plenty of high-income earners live paycheck to paycheck because their spending grows just as fast as their income.

Financial habits shape your future more than occasional big decisions. Choosing to save a little every month, avoiding unnecessary debt, and investing consistently may seem small today, but these habits compound over time.

Think of personal finance like planting a tree. The earlier you start caring for it, the stronger and more rewarding it becomes. Ignore it, and you’ll likely spend years trying to recover from preventable mistakes.

Developing healthy money habits provides more than financial security. It also reduces stress, gives you greater freedom to make life choices, and helps you prepare for unexpected events without panic.

The Hidden Cost of Bad Money Decisions

Financial mistakes often don’t feel expensive in the moment.

Buying a new gadget on impulse, eating out several times a week, or carrying a credit card balance may seem manageable. However, when these behaviors continue month after month, they quietly consume thousands of dollars.

Consider these examples:

| Habit | Monthly Cost | Annual Cost |

|---|---|---|

| Daily coffee ($5) | $150 | $1,800 |

| Impulse online shopping | $200 | $2,400 |

| Unused subscriptions | $40 | $480 |

| Credit card interest | $120 | $1,440 |

Small expenses aren’t always the problem. The real issue is spending without intention.

Successful people don’t necessarily avoid spending—they spend purposefully.

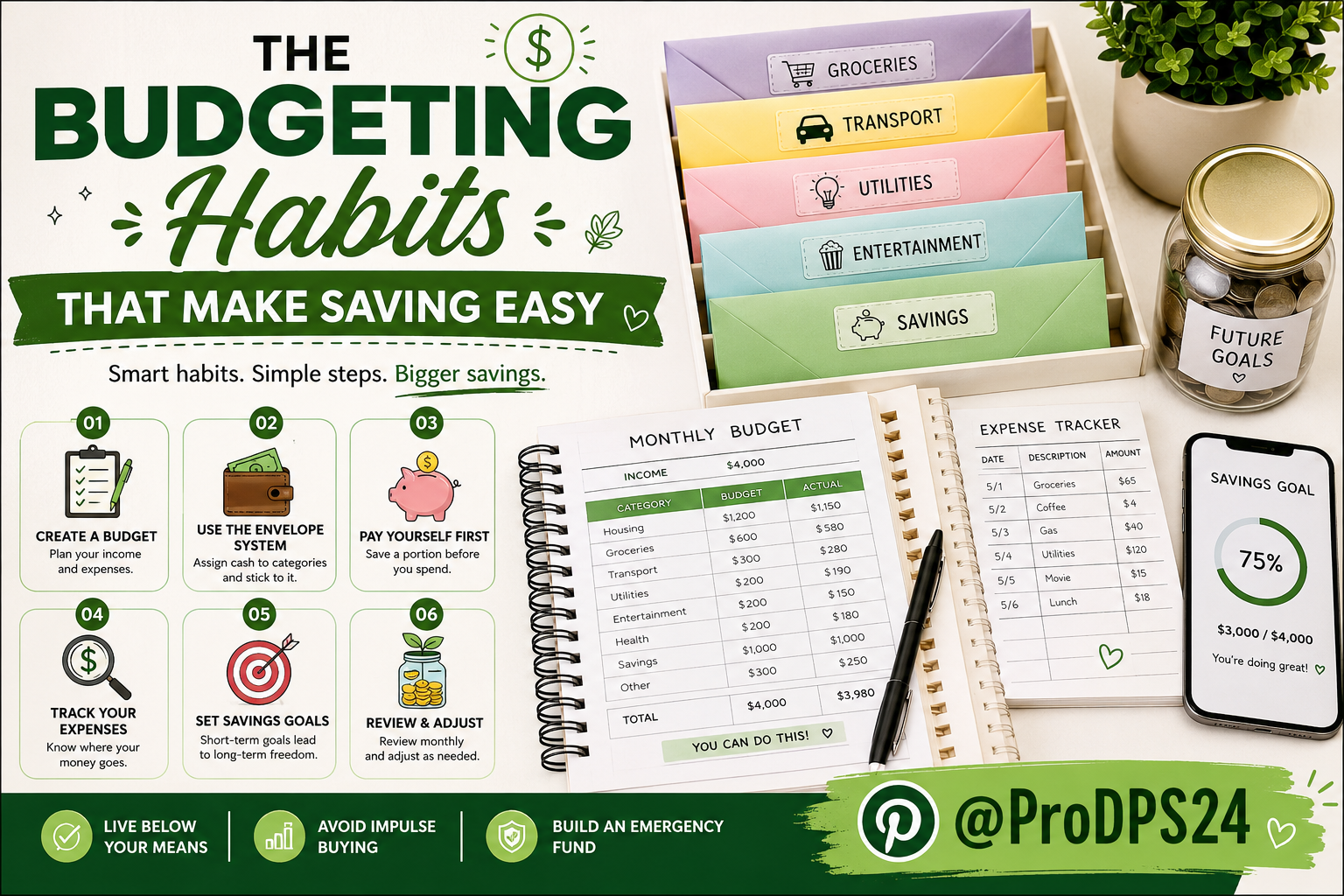

Money Mistake #1: Living Without a Budget

One of the biggest reasons people stay broke is simply not knowing where their money goes.

Without a budget, it’s easy to underestimate expenses and overspend on non-essential purchases. Many people are shocked when they review their bank statements and realize how much they’ve spent on food delivery, subscriptions, or impulse purchases.

Why this happens

People often think budgeting is restrictive or complicated.

In reality, a budget is simply a plan for your money before you spend it.

It helps answer questions like:

- How much should I save?

- How much can I spend guilt-free?

- Am I living within my means?

- Where can I cut unnecessary expenses?

Signs you need a budget

- You run out of money before payday.

- Your savings never seem to grow.

- You don’t know how much you spent last month.

- You rely on credit cards for regular expenses.

- Unexpected bills create financial stress.

Better habit

Create a monthly budget using any method that works for you.

Popular budgeting methods include:

- The 50/30/20 Rule

- Zero-Based Budgeting

- Envelope Budgeting

- Pay Yourself First

The best budget isn’t the most complicated one—it’s the one you’ll actually follow.

Quick Tip

Review your spending every Sunday for just 15 minutes. Small weekly adjustments prevent major monthly problems.

Money Mistake #2: Depending Too Much on Credit Cards

Credit cards are powerful financial tools—but only when used responsibly.

Unfortunately, many people use them to finance lifestyles they can’t actually afford.

This creates a dangerous cycle:

Purchase → Minimum Payment → Interest → Larger Balance → More Debt

Over time, interest charges become one of the biggest obstacles to building wealth.

Common credit card mistakes

- Carrying balances every month

- Paying only the minimum amount due

- Using credit for everyday living expenses

- Opening multiple cards unnecessarily

- Missing payment deadlines

Why it’s harmful

Imagine carrying a $5,000 balance with a high interest rate.

If you only make minimum payments, you could spend years paying it off while paying thousands in interest.

That’s money that could have gone toward investments, savings, or paying down your mortgage.

Better habit

Instead:

- Pay your balance in full each month.

- Keep your credit utilization below 30%.

- Use credit cards for convenience—not borrowing.

- Enable automatic payments to avoid late fees.

Responsible credit use builds a strong credit score while avoiding unnecessary debt.

Money Mistake #3: Impulse Shopping

Modern shopping has never been easier.

With one-click purchases, flash sales, influencer marketing, and constant online advertising, it’s incredibly easy to spend money without thinking.

Most impulse purchases aren’t made because people need something.

They’re made because of emotion.

Stress.

Boredom.

Excitement.

Fear of missing out.

Ask yourself before buying

- Do I truly need this?

- Will I still want it next week?

- Can I comfortably afford it?

- Does this purchase move me closer to my financial goals?

The 24-Hour Rule

One of the simplest ways to reduce unnecessary spending is the 24-hour rule.

Wait one full day before purchasing anything that’s not essential.

You’ll often discover that the urge disappears.

Better habit

Replace emotional spending with intentional spending.

Instead of asking:

“Can I afford this?”

Ask:

“Is this the best use of my money?”

That small mindset shift can save thousands over your lifetime.

Money Mistake #4: Not Building an Emergency Fund

Life is unpredictable.

Cars break down.

Jobs change.

Medical emergencies happen.

Unexpected home repairs appear without warning.

Without emergency savings, these situations often lead to expensive debt.

Why an emergency fund matters

An emergency fund acts as a financial safety net.

Instead of relying on high-interest loans or credit cards, you already have money set aside for genuine emergencies.

How much should you save?

A common recommendation is:

- Beginners: $1,000 starter fund

- Intermediate goal: Three months of living expenses

- Long-term goal: Six months of expenses

If you’re self-employed or have variable income, consider saving even more.

Better habit

Treat savings like a monthly bill.

Set up an automatic transfer every payday—even if it’s only a small amount.

Consistency matters far more than the amount when you’re getting started.

Money Mistake #5: Lifestyle Inflation

One of the most overlooked financial traps is lifestyle inflation.

It happens when your spending increases every time your income increases.

You receive a raise.

Instead of saving or investing the extra money, you upgrade your apartment, buy a more expensive car, eat out more often, or purchase luxury items.

Before long, you’re earning significantly more but still have little or nothing left to save.

Examples of lifestyle inflation

- Upgrading your phone every year without necessity.

- Leasing a more expensive car after getting a raise.

- Moving into a larger home than you actually need.

- Increasing entertainment and dining expenses simply because you earn more.

- Buying premium versions of everything out of habit.

None of these purchases are inherently bad. The problem arises when higher income automatically leads to higher spending.

Better habit

Whenever your income increases:

- Save at least 50% of the raise.

- Increase retirement or investment contributions.

- Pay off outstanding debt faster.

- Build your emergency fund.

- Invest in skills that can grow your future income.

This strategy allows your wealth to grow instead of your monthly expenses.

Real-World Example

Imagine receiving a $500 monthly raise.

Option A: Spend the entire amount on lifestyle upgrades.

Option B: Invest $300 each month and enjoy the remaining $200.

Over many years, the second option has the potential to build substantial wealth through consistent investing and compounding returns.

Money Mistake #6: Ignoring Investing

One of the biggest misconceptions about investing is believing you need a lot of money to get started.

In reality, time is often more important than the amount you invest. Even small, consistent investments can grow significantly thanks to compound growth.

Many people delay investing because they think:

- “I’ll start when I earn more.”

- “Investing is too risky.”

- “I don’t know enough.”

- “I’m too young.”

- “I’m too old.”

Unfortunately, waiting often becomes the most expensive financial mistake.

Why Investing Matters

Saving money protects your wealth.

Investing helps grow it.

If your money sits in a regular savings account for years, inflation gradually reduces its purchasing power. Investing gives your money the opportunity to outpace inflation over the long term.

Beginner-Friendly Investment Options

Depending on your country and financial situation, beginners often consider:

- Broad market index funds

- ETFs (Exchange-Traded Funds)

- Retirement accounts

- Dividend-paying stocks

- Government bonds

- High-yield savings accounts for short-term goals

Every investment carries some level of risk, so it’s important to research your options and choose investments that match your goals and risk tolerance.

Better Habit

Start investing as early as possible—even if it’s only a small amount each month.

Consistency usually matters more than trying to perfectly time the market.

Money Mistake #7: Paying Only the Minimum Balance

Credit card companies are happy when customers pay only the minimum amount.

Why?

Because it keeps debt around longer and generates more interest.

Many people mistakenly believe they’re making good progress by paying the minimum each month. In reality, much of that payment often goes toward interest instead of reducing the balance.

Example

Imagine a credit card balance of:

- Balance: $4,000

- Interest Rate: 22% APR

- Minimum Payment: 2%

Paying only the minimum could take many years to eliminate the debt while costing thousands in additional interest.

Better Habit

Whenever possible:

- Pay more than the minimum.

- Make extra payments throughout the month.

- Focus on high-interest balances first.

- Avoid adding new purchases while paying off debt.

Every extra dollar paid toward the principal reduces future interest costs.

Money Mistake #8: Not Tracking Monthly Expenses

Many people know approximately how much they earn.

Far fewer know exactly where their money goes.

Without expense tracking, it’s almost impossible to identify spending leaks.

Small recurring expenses often have the biggest long-term impact.

Common Hidden Expenses

- Streaming subscriptions

- Mobile app purchases

- Food delivery fees

- Bank fees

- Online memberships

- Daily convenience purchases

Individually, these expenses seem small.

Together, they may total hundreds or even thousands of dollars each year.

Better Habit

Track every expense for one month.

You don’t need expensive software.

You can use:

- A spreadsheet

- A notebook

- Your banking app

- A budgeting app

After one month, categorize every expense.

You’ll likely discover spending patterns you never noticed before.

Money Mistake #9: Waiting Too Long to Save for Retirement

Retirement can feel far away—especially if you’re in your twenties or thirties.

That’s exactly why many people delay planning for it.

The challenge is that time is one of the most valuable assets in retirement planning.

Someone who starts investing early often needs to contribute much less than someone who waits ten or twenty years.

Why Time Matters

Compound growth means your investment earnings can generate additional earnings over time.

The earlier you begin, the longer your money has to grow.

Waiting doesn’t just reduce potential returns—it often requires much larger monthly contributions later in life to reach the same financial goal.

Better Habit

Start now.

Even if you can only contribute a modest amount each month, developing the habit of consistent retirement saving is one of the smartest financial decisions you can make.

Money Mistake #10: Never Learning About Personal Finance

Schools teach many valuable subjects.

Unfortunately, practical money management is often not one of them.

As a result, many adults begin earning income without understanding:

- Budgeting

- Taxes

- Credit scores

- Investing

- Insurance

- Debt management

- Financial planning

This knowledge gap causes many avoidable financial mistakes.

Why Financial Education Matters

Financial literacy helps you:

- Make informed decisions.

- Avoid costly scams.

- Build long-term wealth.

- Reduce financial stress.

- Achieve financial independence.

Learning about money isn’t a one-time event.

It’s an ongoing skill that improves with practice.

Ways to Improve Financial Knowledge

- Read personal finance books.

- Follow reputable financial educators.

- Listen to educational podcasts.

- Take free online finance courses.

- Read trusted financial websites.

- Stay informed about basic investing principles.

The more you understand money, the more confident your financial decisions become.

Building Better Money Habits

Avoiding financial mistakes is only half the equation.

The other half is intentionally creating habits that improve your financial future.

Here are some practical habits that consistently help people build wealth:

Pay Yourself First

Before paying bills or spending money, automatically transfer a portion of each paycheck into savings or investments.

Live Below Your Means

Just because you can afford something doesn’t mean you should buy it.

Keeping your lifestyle modest creates room for saving, investing, and financial flexibility.

Set Clear Financial Goals

Goals give your money a purpose.

Examples include:

- Building a $10,000 emergency fund

- Paying off credit card debt

- Saving for a home

- Investing for retirement

- Starting a business

Write your goals down and review them regularly.

Increase Income Alongside Saving

While controlling expenses is important, increasing your income can accelerate financial progress.

Ideas include:

- Freelancing

- Starting a side business

- Selling digital products

- Learning high-income skills

- Negotiating a raise

- Investing in education

The combination of earning more and spending wisely creates powerful long-term results.

Wealth-Building Habits vs. Wealth-Destroying Habits

| Wealth-Destroying Habit | Wealth-Building Habit |

|---|---|

| Living paycheck to paycheck | Spending less than you earn |

| Impulse buying | Planned purchases |

| Carrying credit card debt | Paying balances in full |

| No emergency fund | Saving consistently |

| Ignoring investments | Investing regularly |

| Lifestyle inflation | Saving raises and bonuses |

| No budget | Monthly financial planning |

| Delaying retirement | Starting early |

| Avoiding financial education | Continuous learning |

| Emotional spending | Goal-based spending |

The Power of Small Financial Changes

One of the most encouraging truths about personal finance is that meaningful progress doesn’t require dramatic changes overnight.

Small improvements, repeated consistently, often lead to the greatest long-term success.

For example:

- Bringing lunch from home a few days a week

- Canceling subscriptions you don’t use

- Saving a percentage of every paycheck

- Paying an extra amount toward debt each month

- Investing consistently over many years

These habits may seem minor individually, but together they can significantly improve your financial health.

Remember, becoming financially secure isn’t about perfection. It’s about making better decisions more often than bad ones.

Part 3: Practical Guide, FAQs & Conclusion

Practical Tips & Actionable Checklist

Learning about money is valuable, but taking action is what creates lasting results. Use this checklist to strengthen your financial habits one step at a time.

✅ Daily Habits

- Track every purchase, even small ones.

- Think before buying anything that isn’t essential.

- Avoid impulse shopping by following the 24-hour rule.

- Compare prices before making major purchases.

- Bring lunch or coffee from home a few times each week.

- Check your bank account regularly to stay aware of your spending.

✅ Weekly Habits

- Review your budget.

- Check upcoming bills.

- Pay off your credit card balance if possible.

- Transfer money into savings or investments.

- Review your financial goals and adjust if necessary.

✅ Monthly Habits

- Save at least 20% of your income whenever possible.

- Update your emergency fund.

- Review subscriptions and cancel unused services.

- Track your net worth.

- Review investment performance without reacting to short-term market changes.

- Plan next month’s budget before the month begins.

✅ Annual Habits

- Increase your savings rate after a raise.

- Review insurance coverage.

- Update retirement contributions.

- Check your credit report.

- Reevaluate your financial goals.

Common Money Mistakes to Avoid

Even people with good intentions can fall into financial traps. Being aware of these pitfalls makes them easier to avoid.

1. Trying to Get Rich Quickly

Promises of guaranteed high returns are often scams or extremely risky investments.

Focus on steady, long-term growth instead.

2. Ignoring Small Expenses

A few dollars here and there may not seem significant, but recurring expenses can quietly consume thousands of dollars each year.

3. Using Debt to Buy Luxuries

Borrowing money for items that quickly lose value can create years of unnecessary financial stress.

4. Copying Other People’s Lifestyle

Social media often highlights luxury lifestyles without showing the debt or financial struggles behind them.

Build your finances based on your own goals—not someone else’s highlight reel.

5. Having No Financial Goals

Without goals, it’s difficult to make intentional spending decisions.

Set clear targets such as:

- Paying off debt

- Buying a home

- Saving for retirement

- Starting a business

- Building passive income

6. Not Preparing for Emergencies

Unexpected expenses are part of life.

An emergency fund helps you avoid turning every surprise into debt.

7. Waiting for the “Perfect Time”

There will never be a perfect moment to start budgeting, saving, or investing.

Starting today—even with a small amount—is usually better than waiting for ideal conditions.

Frequently Asked Questions (FAQs)

1. What is the biggest money mistake people make?

Living beyond their means is one of the most common financial mistakes. Spending more than you earn often leads to debt, financial stress, and limited opportunities to build wealth.

2. Why do many people stay broke even with a good salary?

A high income doesn’t automatically create wealth. Poor budgeting, lifestyle inflation, excessive debt, and a lack of investing can prevent even high earners from becoming financially secure.

3. How much should I save every month?

A common guideline is to save at least 20% of your income if your circumstances allow. However, even saving a smaller percentage consistently is a positive step toward financial stability.

4. Should I pay off debt before investing?

It depends on the type of debt. High-interest debt, such as most credit card balances, is often a priority because the interest can outweigh potential investment returns. Once expensive debt is under control, investing regularly can help grow your wealth over time.

5. How large should an emergency fund be?

A practical goal is three to six months of essential living expenses. If you’re self-employed or have irregular income, you may want to save even more.

6. Is investing risky?

All investments involve some level of risk. However, investing in diversified assets over the long term has historically helped many people build wealth while reducing the impact of short-term market fluctuations.

7. Can I build wealth on an average income?

Yes. Many financially successful people built wealth by consistently budgeting, saving, investing, and avoiding unnecessary debt rather than relying on exceptionally high incomes.

8. What is the fastest way to improve my finances?

Focus on the habits you can control:

- Create a budget.

- Reduce unnecessary spending.

- Pay off high-interest debt.

- Build an emergency fund.

- Invest consistently.

- Continue improving your financial knowledge.

9. What’s the difference between saving and investing?

Saving is generally intended for short-term needs and emergencies, while investing aims to grow your money over the long term. A healthy financial plan often includes both.

10. How long does it take to become financially stable?

Financial stability looks different for everyone. Consistently following good money habits over several years can make a significant difference, even if progress feels gradual at first.

Expert Tips Most People Overlook

Automate Good Decisions

Set up automatic transfers for savings and investments so your financial goals happen without relying on willpower.

Increase Your Savings Every Year

Whenever your income increases, raise your savings or investment contribution before increasing your spending.

Focus on Net Worth, Not Income

Income matters, but your net worth—what you own minus what you owe—is a better indicator of long-term financial health.

Invest in Yourself

Learning valuable skills can increase your earning potential over time. Education, certifications, and practical experience often provide returns that extend far beyond traditional investments.

Review Your Financial Progress Regularly

Schedule a monthly “money meeting” with yourself or your family to review goals, spending, and upcoming financial priorities.

Key Takeaways

- Small financial mistakes can become expensive over time.

- Budgeting helps you control where your money goes.

- Avoid carrying high-interest credit card debt.

- Build an emergency fund before unexpected expenses arise.

- Invest consistently to take advantage of long-term growth.

- Lifestyle inflation can prevent wealth accumulation.

- Financial education is a lifelong investment.

- Small, consistent habits often have a bigger impact than occasional big changes.

- Wealth is built through discipline, patience, and intentional decisions.

Final Conclusion

Financial success isn’t about luck or earning the highest salary. It’s about making thoughtful decisions with the money you already have and building habits that support your long-term goals.

Every positive financial choice—whether it’s creating a budget, paying off debt, building an emergency fund, or investing consistently—moves you closer to financial freedom.

Don’t worry about becoming perfect overnight. Instead, focus on making one better decision today than you did yesterday. Over time, those small improvements can create remarkable results.

Remember, every wealthy person started somewhere. The best time to improve your finances was years ago. The second-best time is today.

If you found this guide helpful, consider sharing it with friends or family who want to improve their finances. You can also save this article to Pinterest for future reference and explore more practical guides, money-saving strategies, and personal finance resources on ProDPS.com.

Small financial habits create big results—start building yours today.

---Advertisement---

[adinserter block="1"]

LATEST post

The Budgeting Habits That Make Saving Easy: 10 Simple Money Habits for Financial Success

July 11, 2026

4:03 am

20 Best Printable Products to Sell Online (High-Demand Ideas for 2026)

July 10, 2026

5:49 am

15 Best Free AI Websites You Should Bookmark in 2026

July 10, 2026

5:27 am

18 Side Hustles That Require Almost No Money (Beginner Guide)

July 9, 2026

5:08 pm

Money Mistakes That Keep People Broke (And How to Avoid Them)

July 9, 2026

4:28 pm