Small Money Changes That Can Transform Your Future

When people think about becoming financially successful, they often imagine earning a much higher salary, winning the lottery, or launching a million-dollar business. While those events certainly change lives, they’re not the path most financially secure people follow.

Real financial success usually comes from consistent, intentional decisions made over months and years. Small improvements in how you earn, spend, save, and invest can create remarkable results through the power of consistency.

Imagine saving just a few dollars each day instead of spending them impulsively. Over time, those seemingly insignificant amounts can become an emergency fund, an investment portfolio, or even the down payment on a home.

The good news is that you don’t need to completely change your lifestyle overnight. Instead, you can focus on simple habits that gradually improve your financial health while remaining realistic and sustainable.

In this guide, you’ll discover practical money habits that anyone can start today. Whether you’re just beginning your financial journey or looking to strengthen your current strategy, these small changes can help you create a stronger, more secure financial future.

Why Small Money Changes Matter More Than Big Financial Decisions

Many people wait for the “perfect moment” to improve their finances. They tell themselves they’ll start saving after getting a raise, paying off debt, or finding a better job.

Unfortunately, waiting often becomes a lifelong habit.

Financial improvement rarely begins with a dramatic event. Instead, it grows through small decisions repeated consistently.

Think about two people:

Person A

- Saves $10 every day.

- Reviews spending weekly.

- Avoids unnecessary impulse purchases.

- Invests regularly.

Person B

- Earns slightly more money.

- Spends without tracking expenses.

- Saves only occasionally.

- Delays investing.

After several years, Person A often ends up in a stronger financial position despite earning less. That’s because financial success is driven by habits more than income alone.

The Compound Effect

Small improvements create momentum.

Saving an extra $5 today may not seem important, but doing it every day for years can produce meaningful financial growth—especially when those savings are invested and allowed to compound over time.

Consistency beats intensity.

Instead of making drastic financial changes for one month and quitting, focus on sustainable habits you can maintain for years.

The Psychology Behind Better Money Decisions

Money is emotional.

Many purchases aren’t based on need—they’re driven by stress, excitement, boredom, advertising, or social pressure.

Understanding why you spend is often more important than knowing how much you spend.

Recognize Emotional Spending

Ask yourself before buying something:

- Do I actually need this?

- Will I still value it next month?

- Is this solving a real problem?

- Am I buying because of stress or boredom?

These simple questions can prevent many unnecessary purchases.

Replace Instant Gratification

Modern technology makes spending incredibly easy.

With one click, money disappears.

Successful savers learn to delay gratification.

Instead of asking:

“Can I afford this?”

Ask:

“Is this the best use of my money?”

This small mindset shift often leads to smarter financial choices.

Focus on Progress, Not Perfection

Nobody manages money perfectly.

Unexpected expenses happen.

Budgets sometimes fail.

The goal isn’t perfection—it’s continuous improvement.

Missing one saving goal shouldn’t stop you from continuing the next day.

Small progress repeated consistently is what builds lasting wealth.

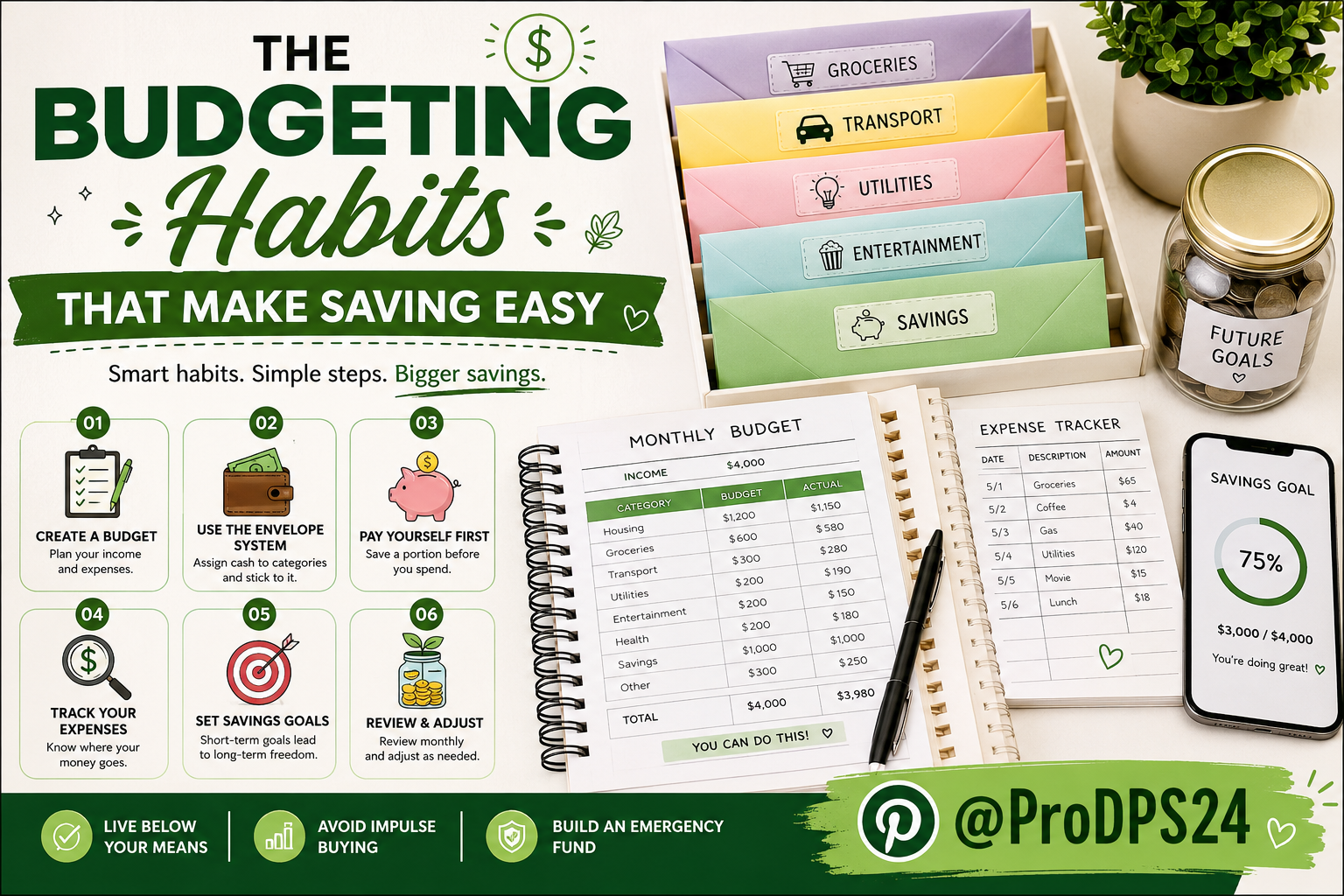

Build a Budget That Actually Works

Many people dislike budgeting because they think it means giving up everything they enjoy.

A good budget does the opposite.

It gives every dollar a purpose while still allowing room for entertainment, hobbies, and personal goals.

Know Where Your Money Goes

Before creating a budget, track every expense for one month.

You might be surprised by where your money actually goes.

Common categories include:

- Housing

- Utilities

- Transportation

- Food

- Insurance

- Entertainment

- Shopping

- Subscriptions

- Healthcare

- Savings

Once you understand your spending habits, making improvements becomes much easier.

Use Simple Budget Categories

A budget doesn’t need to be complicated.

Start with broad categories instead of dozens of tiny ones.

For example:

| Category | Purpose |

|---|---|

| Needs | Rent, groceries, utilities |

| Wants | Dining out, entertainment, hobbies |

| Savings | Emergency fund, investments, future goals |

This approach keeps budgeting manageable and easier to maintain.

Review Your Budget Weekly

Financial plans shouldn’t sit in a drawer.

Spend 10–15 minutes each week reviewing:

- Recent spending

- Bills coming due

- Savings progress

- Upcoming expenses

Weekly reviews help catch small problems before they become expensive ones.

Create Daily Saving Habits

Saving money doesn’t require dramatic sacrifices.

Instead, look for opportunities to make small improvements every day.

Pay Yourself First

Many people save whatever remains at the end of the month.

Unfortunately, very little is usually left.

Instead, move money into savings immediately after receiving your income.

Treat saving like a non-negotiable bill.

Challenge Small Daily Expenses

Small purchases can quietly reduce your ability to build wealth.

Examples include:

- Frequent takeout meals

- Impulse online shopping

- Unused subscriptions

- Convenience purchases

- Premium delivery fees

You don’t need to eliminate everything.

Simply reducing unnecessary spending creates room for meaningful savings over time.

Set Specific Savings Goals

Saving becomes easier when your money has a purpose.

Examples include:

- Emergency fund

- Vacation

- New laptop

- Education

- Home purchase

- Retirement

- Business investment

People are generally more motivated when they know exactly what they’re working toward.

Spend More Intentionally Instead of Spending Less

Many financial experts focus on cutting expenses, but long-term success isn’t about depriving yourself. It’s about making intentional choices with your money.

Intentional spending means directing your money toward the things that genuinely improve your life while reducing purchases that don’t provide lasting value.

For example, spending money on education, professional development, quality tools, or experiences with family may provide far greater long-term value than frequent impulse purchases.

Before making any non-essential purchase, ask yourself:

- Will this still make me happy six months from now?

- Does this purchase align with my financial goals?

- Could this money serve a better purpose?

- Am I buying because I need it or because it’s convenient?

These simple questions can dramatically improve your spending habits.

Differentiate Needs from Wants

One of the easiest ways to improve your finances is learning the difference between essential expenses and discretionary spending.

| Needs | Wants |

|---|---|

| Rent or mortgage | Designer clothing |

| Utilities | Premium streaming subscriptions |

| Groceries | Daily restaurant meals |

| Insurance | Luxury gadgets |

| Transportation to work | Frequent impulse shopping |

This doesn’t mean eliminating all “wants.” Instead, enjoy them intentionally after your essential financial priorities are covered.

Practice the 24-Hour Rule

Impulse purchases are one of the biggest obstacles to saving money.

Whenever you’re tempted to buy something that isn’t essential, wait at least 24 hours before completing the purchase.

During that waiting period, you’ll often discover that the excitement fades, making it much easier to decide whether the purchase is truly worthwhile.

For larger purchases, consider extending the waiting period to 7–30 days.

Avoid Lifestyle Inflation

As income increases, many people automatically increase their spending.

A raise often leads to:

- A larger apartment

- A newer car

- More expensive vacations

- Luxury subscriptions

- Higher monthly bills

While enjoying your success is important, increasing your expenses as fast as your income makes it difficult to build wealth.

Instead, try this strategy:

Whenever you receive a raise or bonus:

- Save 50%

- Invest 30%

- Spend 20%

This allows you to enjoy your progress while steadily improving your financial future.

Build an Emergency Fund Before You Need It

Unexpected expenses happen to everyone.

A medical bill, vehicle repair, home maintenance issue, or temporary job loss can quickly become overwhelming if you’re financially unprepared.

An emergency fund acts as your financial safety net.

Instead of relying on credit cards or loans during emergencies, you can confidently handle unexpected situations using money you’ve already saved.

Why an Emergency Fund Matters

An emergency fund provides:

- Peace of mind

- Financial stability

- Reduced stress

- Protection from debt

- Greater flexibility during difficult times

Even a modest emergency fund can prevent a temporary setback from becoming a long-term financial crisis.

How Much Should You Save?

Your savings target depends on your financial situation.

A simple guideline is:

| Situation | Recommended Emergency Fund |

|---|---|

| Beginner | $500–$1,000 |

| Stable employment | 3 months of expenses |

| Freelancers or business owners | 6–12 months of expenses |

Don’t worry about reaching the final goal immediately.

Start with your first $500, then your first $1,000, and continue building from there.

Keep Emergency Savings Separate

Your emergency fund should be easy to access—but not so convenient that you’re tempted to spend it.

Many people keep emergency savings in a separate high-yield savings account.

This separation helps reduce unnecessary withdrawals while allowing quick access during genuine emergencies.

Rebuild After Using It

If an emergency occurs, remember that using the fund is not a failure.

That’s exactly what it was created for.

After the emergency has passed, make rebuilding your savings one of your top financial priorities.

Start Investing Earlier Than You Think

One of the most common financial regrets is waiting too long to begin investing.

Many people believe they need thousands of dollars before getting started.

In reality, consistency matters much more than starting with a large amount.

Investing allows your money to work for you through long-term growth and compound returns.

The earlier you begin, the more time your investments have to grow.

Understand Compound Growth

Compound growth occurs when your investment earnings begin generating additional earnings.

Imagine planting a small tree.

At first, growth seems slow.

Over time, however, the tree becomes stronger, larger, and more productive.

Investments work in a similar way.

The longer they remain invested, the greater the opportunity for long-term growth.

This is why starting early—even with small amounts—can make a significant difference over many years.

Start With What You Can Afford

You don’t need to invest hundreds of dollars every month.

Even modest, consistent contributions can build momentum.

Examples include:

- Investing a portion of each paycheck

- Contributing monthly instead of occasionally

- Increasing investments after receiving raises

- Reinvesting investment earnings

The habit of investing consistently is often more valuable than trying to time the market perfectly.

Diversify Your Investments

Avoid putting all your money into one investment.

Diversification helps reduce risk by spreading your investments across different assets.

Possible investment categories include:

- Broad stock market funds

- Bonds

- Retirement accounts

- Real estate investments

- Cash savings

Diversification doesn’t eliminate risk, but it can help create a more balanced long-term investment strategy.

Think Long Term

Markets naturally rise and fall.

Short-term fluctuations are normal.

Successful investors focus on long-term goals instead of reacting emotionally to daily market movements.

Patience is one of the most valuable investing skills you can develop.

Automate Your Financial Success

One of the easiest ways to improve your finances is removing the need to make constant decisions.

Automation helps ensure important financial tasks happen consistently.

Instead of relying on motivation every month, create systems that work automatically.

Automate Savings

Set up automatic transfers from your checking account to your savings account.

Even small weekly or monthly transfers gradually build meaningful savings.

Automation removes the temptation to spend money before saving it.

Automate Investing

Many investment platforms allow recurring contributions.

This strategy helps you:

- Invest consistently

- Reduce emotional decision-making

- Build wealth gradually

- Stay committed to long-term goals

Consistency often matters more than trying to predict market movements.

Automate Bill Payments

Late payment fees can quietly reduce your financial progress.

Automatic bill payments help you:

- Avoid unnecessary penalties

- Improve payment consistency

- Protect your financial reputation

- Reduce monthly stress

Always keep enough funds available to prevent overdrafts.

Schedule Monthly Financial Reviews

Automation doesn’t replace financial awareness.

Once each month, spend 20–30 minutes reviewing:

- Income

- Expenses

- Savings progress

- Investment contributions

- Debt balances

- Financial goals

These short reviews help you identify opportunities for improvement before small issues become larger problems.

Practical Money Checklist

Use this checklist to strengthen your financial habits.

Daily Checklist

- Track your spending.

- Avoid impulse purchases.

- Review unnecessary expenses.

- Save a small amount.

- Think before making discretionary purchases.

Weekly Checklist

- Review your budget.

- Compare planned versus actual spending.

- Update savings progress.

- Check upcoming bills.

- Adjust your budget if needed.

Monthly Checklist

- Pay all bills on time.

- Increase savings whenever possible.

- Review investment contributions.

- Evaluate subscriptions.

- Monitor financial goals.

- Celebrate progress, even small wins.

Yearly Checklist

- Review your financial goals.

- Evaluate insurance coverage.

- Check investment performance.

- Update your emergency fund target.

- Plan savings goals for the coming year.

- Reflect on lessons learned and set new financial priorities.

Remember, financial success is rarely the result of one perfect decision. It’s the outcome of hundreds of thoughtful choices made consistently over time.

Common Money Mistakes That Can Slow Your Financial Progress

Building wealth isn’t only about making smart decisions—it’s also about avoiding common mistakes that quietly drain your finances over time. Fortunately, most of these mistakes can be corrected with awareness and consistency.

1. Living Without a Budget

Without a budget, it’s difficult to know where your money is going. Many people underestimate how much they spend on small purchases, subscriptions, or convenience items.

Better approach: Create a simple monthly budget and review it regularly. Your budget should be flexible enough to adapt as your financial situation changes.

2. Ignoring Small Daily Expenses

A single coffee or online purchase may not seem significant, but repeated daily expenses can add up over months and years.

Better approach: Track recurring small expenses. You don’t need to eliminate every treat—just make sure your spending aligns with your priorities.

3. Not Saving for Emergencies

Unexpected expenses are inevitable. Without an emergency fund, even a minor setback can lead to debt.

Better approach: Start with a realistic goal, such as saving your first $500 or $1,000, then continue building toward several months of essential living expenses.

4. Delaying Investing

Many people postpone investing because they think they need a large amount of money or perfect market timing.

Better approach: Focus on consistent investing over time. Starting early often has a greater impact than starting with a larger amount later.

5. Carrying High-Interest Debt

High-interest debt can make it difficult to achieve other financial goals because interest charges reduce the money available for saving and investing.

Better approach: Prioritize paying off high-interest balances while continuing to build healthy financial habits.

6. Comparing Yourself to Others

Social media and advertising often encourage unnecessary spending to keep up with other people’s lifestyles.

Better approach: Measure success by your own goals, not by someone else’s spending habits.

7. Failing to Review Financial Progress

Many people create a budget or savings plan and never look at it again.

Better approach: Schedule regular financial check-ins to review your progress, celebrate milestones, and make adjustments when needed.

Expert Tips for Building Long-Term Wealth

Financial success doesn’t require perfection. It requires consistency, patience, and thoughtful decision-making. These expert tips can help you stay on track.

Prioritize Consistency Over Perfection

Missing one savings goal or making an unnecessary purchase doesn’t erase your progress. Return to your plan and keep moving forward.

Increase Savings When Income Grows

Whenever you receive a raise, bonus, or additional income, consider directing part of it toward savings or investments before increasing your spending.

Continue Learning About Personal Finance

Financial knowledge is one of the best investments you can make. Read books, follow reputable financial educators, and stay informed about budgeting, investing, and long-term planning.

Review Your Financial Goals Regularly

Your goals will change as your life changes. Marriage, homeownership, career growth, or starting a business may require adjustments to your financial plan.

Celebrate Milestones

Reaching your first savings goal, paying off debt, or consistently following a budget deserves recognition. Celebrating progress helps reinforce positive financial habits.

Frequently Asked Questions (FAQs)

1. What are small money changes?

Small money changes are simple financial habits—such as tracking expenses, saving consistently, avoiding impulse purchases, and investing regularly—that can improve your financial future over time.

2. Can small savings really make a difference?

Yes. Consistent saving, even in modest amounts, can grow significantly over time, especially when combined with long-term investing and compound growth.

3. How much should I save each month?

The ideal amount depends on your income and expenses. The most important step is to save consistently, even if you start with a small percentage of your income.

4. Should I pay off debt before investing?

It depends on the type of debt. High-interest debt is often a priority, while some people choose to balance debt repayment with regular investing. Consider your personal financial situation and goals.

5. Do I need a complicated budget?

No. A simple budget that tracks income, essential expenses, discretionary spending, and savings is often easier to maintain than an overly detailed one.

6. How often should I review my finances?

A quick weekly review and a more detailed monthly review can help you stay organized and make informed financial decisions.

7. What is the first financial goal I should focus on?

Many people begin by creating a small emergency fund while developing consistent budgeting and saving habits.

8. Is it too late to improve my financial future?

No. While starting early provides advantages, improving your financial habits at any stage of life can lead to meaningful long-term benefits.

9. How can I avoid impulse spending?

Try using a waiting period before making non-essential purchases, unsubscribe from promotional emails that encourage unnecessary spending, and shop with a list whenever possible.

10. What is the most important financial habit?

Consistency. Regular budgeting, saving, and thoughtful spending often have a greater long-term impact than occasional major financial decisions.

Key Takeaways

- Small daily financial habits can produce meaningful long-term results.

- Budgeting gives every dollar a purpose.

- Saving consistently is more important than saving large amounts occasionally.

- An emergency fund provides financial security during unexpected situations.

- Investing early allows compound growth to work in your favor.

- Intentional spending helps align your money with your priorities.

- Automating savings and investments can simplify wealth building.

- Regular financial reviews help you stay on track and adjust your goals as needed.

- Avoid comparing your financial journey to others.

- Long-term consistency is the foundation of lasting financial success.

Final Conclusion

Transforming your financial future doesn’t require extraordinary income, perfect timing, or dramatic lifestyle changes. Instead, it begins with small, intentional choices that you repeat consistently.

Every dollar you save, every thoughtful purchase you make, and every investment you contribute to is a step toward greater financial security. While individual actions may seem insignificant, their combined effect over months and years can be remarkable.

Remember that financial success is a journey rather than a destination. There will be setbacks, unexpected expenses, and changing priorities. What matters most is your willingness to continue learning, adapting, and making steady progress.

By creating a realistic budget, saving consistently, investing for the long term, and reviewing your finances regularly, you’ll build habits that support lasting financial confidence and freedom.

The best time to improve your financial future is not someday—it’s today.

Call to Action

If you found this guide helpful, explore more practical personal finance resources on ProDPS.com. You’ll find additional articles covering budgeting, saving, investing, productivity, and smart money strategies designed to help you make informed financial decisions.

Share this article with friends or family members who want to build stronger financial habits, and bookmark it so you can revisit these strategies as your financial journey evolves.

Remember: lasting wealth is rarely built through one big decision. It’s built through hundreds of smart, consistent choices that begin with the next step you take today.