Why Smart Financial Habits Matter

Money influences nearly every aspect of life, from the home you live in to the opportunities you can pursue. While earning more income can certainly help, lasting financial success is usually the result of consistent habits rather than occasional big decisions.

Smart financial habits provide a strong foundation that helps you:

- Stay in control of your spending

- Reduce financial stress

- Prepare for unexpected emergencies

- Reach savings goals faster

- Avoid unnecessary debt

- Build wealth steadily over time

- Gain confidence when making financial decisions

Many people believe they need a large salary to become financially secure. In reality, someone with average earnings and excellent money habits can often achieve greater financial stability than someone with a high income but poor spending habits.

Think of your finances like your physical health. Small daily choices—saving a little, avoiding impulse purchases, and following a budget—may seem insignificant at first. Over months and years, those choices create remarkable results.

The earlier you develop healthy financial habits, the more time you give your money to grow. Thanks to compound growth, even modest savings can increase significantly over the long term when managed wisely.

Understand Your Income and Expenses

Before improving your finances, you need a clear picture of where your money comes from and where it goes. Many people underestimate how much they spend because they don’t track everyday purchases.

Understanding your cash flow is the first step toward better money management.

Track Every Dollar

For one full month, record every expense, no matter how small.

Include:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Dining out

- Online shopping

- Entertainment

- Subscriptions

- Coffee and snacks

- Miscellaneous purchases

You can use:

- A budgeting app

- A spreadsheet

- A notebook

- Your banking app

- Expense tracking software

Tracking every purchase creates awareness, and awareness often leads to better decisions without requiring major lifestyle changes.

Example

Imagine buying a $6 coffee every weekday.

- Daily: $6

- Weekly: $30

- Monthly: Around $130

- Yearly: Over $1,500

This doesn’t mean you should never buy coffee—it simply helps you understand where your money is going and decide whether the expense aligns with your priorities.

Identify Spending Patterns

Once you’ve tracked your expenses, look for trends.

Ask yourself:

- Where am I spending the most money?

- Which expenses are essential?

- Which purchases could be reduced?

- Are there subscriptions I no longer use?

- How often do I make impulse purchases?

Many beginners are surprised to discover that small recurring expenses add up faster than occasional large purchases.

Common spending leaks include:

- Multiple streaming services

- Food delivery fees

- Unused gym memberships

- Frequent online shopping

- Convenience purchases

Finding these patterns allows you to redirect money toward your savings and financial goals instead.

Create Financial Awareness

Financial awareness means understanding your current financial situation without guessing.

Know your:

- Monthly income

- Fixed expenses

- Variable expenses

- Total savings

- Outstanding debt

- Credit obligations

- Financial goals

Review your finances at least once each month. Regular check-ins help you catch problems early and stay focused on your long-term objectives.

Remember, you can’t improve what you don’t measure.

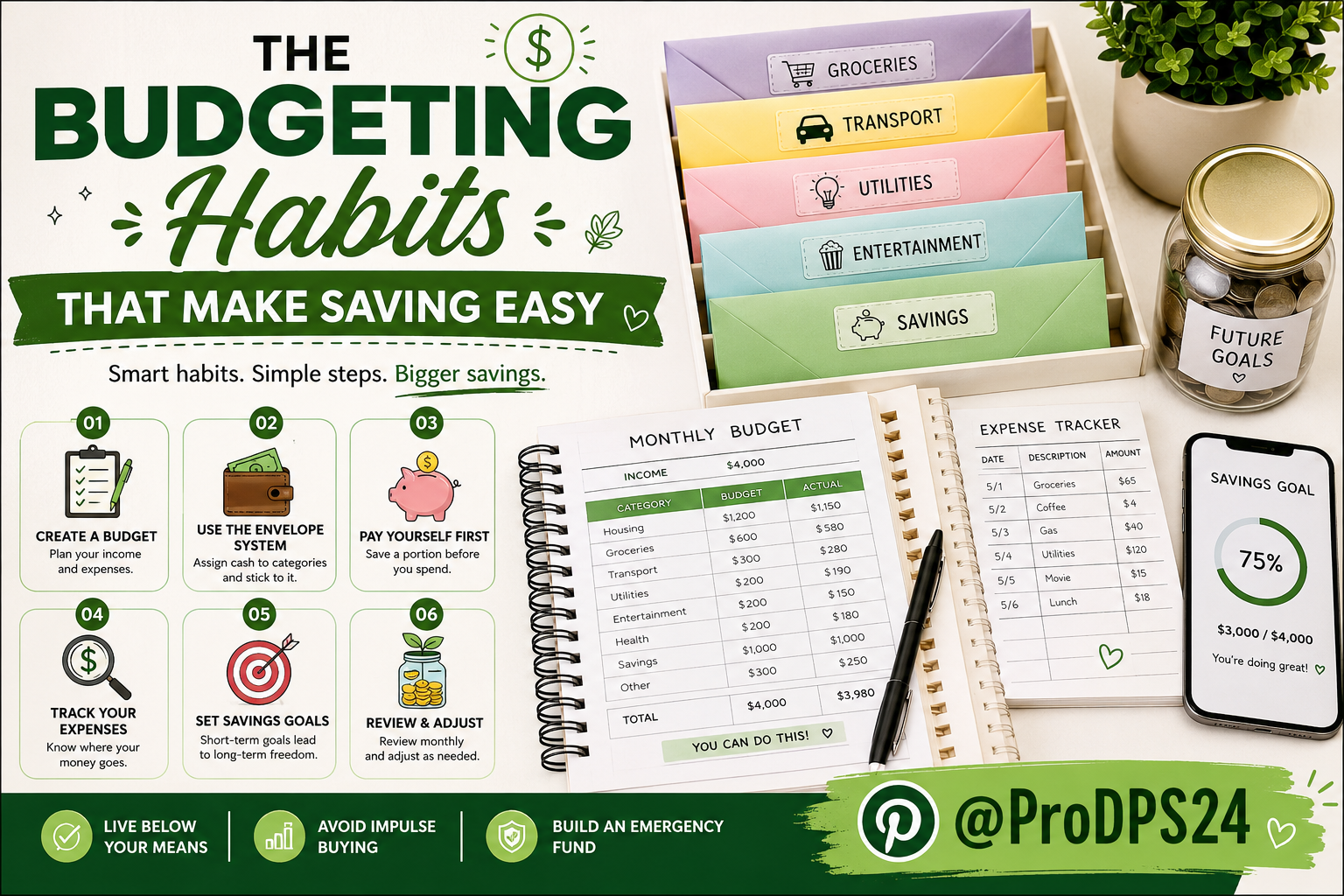

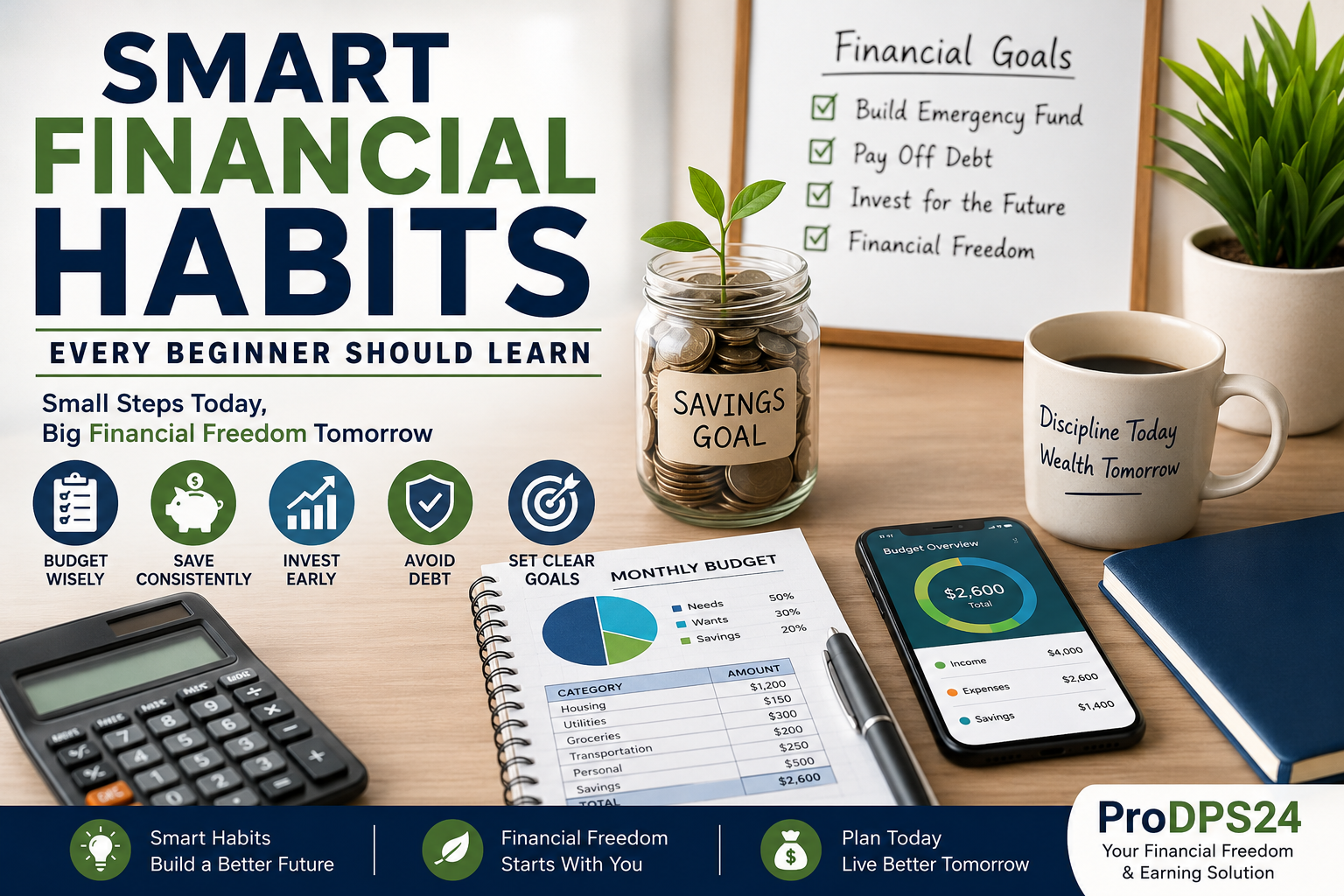

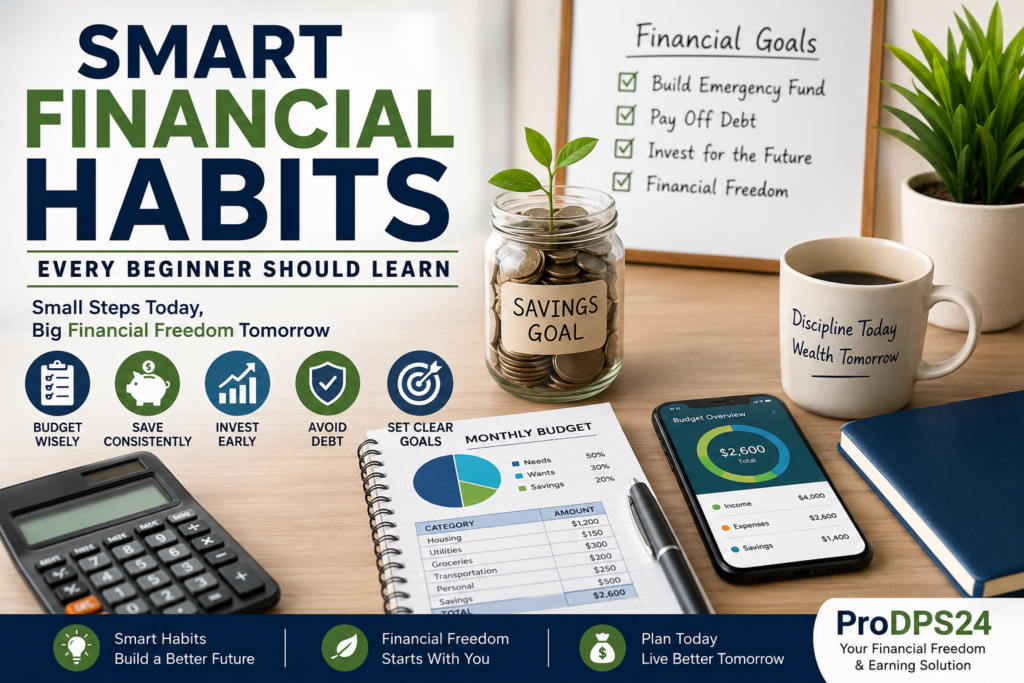

Build a Realistic Monthly Budget

A budget isn’t about restricting yourself—it’s about giving every dollar a purpose. A well-planned budget helps ensure that your income supports your priorities instead of disappearing on unnecessary expenses.

The best budget is one you can realistically maintain.

Choose a Budgeting Method

There isn’t a single budgeting system that works for everyone. Select one that matches your lifestyle and financial goals.

The 50/30/20 Rule

One of the most popular budgeting methods divides your after-tax income into three categories:

- 50% for essential needs such as housing, groceries, transportation, insurance, and utilities.

- 30% for personal wants like entertainment, travel, hobbies, and dining out.

- 20% for savings, investments, and debt repayment.

This method is easy to follow and provides flexibility while encouraging consistent saving.

Zero-Based Budget

With a zero-based budget, every dollar of income is assigned a job.

Income – Expenses – Savings = Zero

This doesn’t mean your bank account reaches zero. It means every dollar has a planned purpose before the month begins.

People who enjoy detailed planning often find this budgeting style highly effective.

Pay Yourself First

Instead of saving whatever money is left at the end of the month, save first.

For example:

- Receive paycheck

- Transfer money into savings immediately

- Pay bills

- Spend what’s left according to your budget

This simple habit dramatically increases long-term savings because it removes the temptation to spend first.

Prioritize Essential Expenses

When building your budget, cover necessities before discretionary spending.

Typical priorities include:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Debt payments

- Emergency savings

After these essentials are covered, you can allocate money toward entertainment, travel, shopping, and other lifestyle expenses.

Prioritizing needs over wants doesn’t eliminate enjoyment—it simply ensures your financial responsibilities are met first.

Adjust Your Budget Regularly

Life changes, and your budget should change with it.

Review your budget every month to account for:

- Salary increases

- New bills

- Seasonal expenses

- Inflation

- Family changes

- Financial goals

Budgeting isn’t something you create once and forget. It’s an ongoing process that evolves as your life changes.

Even small monthly adjustments can keep your finances on track and help you avoid overspending.

By treating your budget as a flexible financial roadmap rather than a strict set of rules, you’ll be much more likely to stick with it over the long term.

Save Money Before You Spend

One of the biggest differences between people who struggle financially and those who build long-term wealth is the habit of saving consistently. Many beginners make the mistake of waiting until the end of the month to save whatever money is left. Unfortunately, there is often very little—or nothing—remaining.

A smarter strategy is to save first and spend later. This approach, often called “Pay Yourself First,” makes saving a priority instead of an afterthought.

By treating savings like a monthly bill, you gradually build financial security without relying on willpower alone.

Pay Yourself First

As soon as your paycheck arrives, move a portion into your savings account before paying for optional expenses.

For example:

- Monthly Income: $3,000

- Savings: $300 (10%)

- Remaining Budget: $2,700

Even if you start by saving only 5%, consistency is more important than the amount. As your income grows, increase your savings rate whenever possible.

Automate Your Savings

Automation removes the temptation to spend money that should be saved.

You can automate:

- Transfers to a savings account

- Retirement contributions

- Investment deposits

- Emergency fund contributions

When savings happen automatically, building wealth becomes much easier because you don’t have to remember to do it every month.

Build an Emergency Fund

Unexpected expenses are a normal part of life.

Examples include:

- Car repairs

- Medical bills

- Home maintenance

- Job loss

- Family emergencies

- Unexpected travel

Without emergency savings, many people rely on high-interest credit cards or loans.

A good starting goal is to save:

- First Goal: $500–$1,000

- Next Goal: Three months of living expenses

- Long-Term Goal: Six months of essential expenses

An emergency fund provides peace of mind and protects your long-term financial goals from temporary setbacks.

Make Saving a Habit

Saving doesn’t have to involve large amounts.

Simple habits include:

- Rounding up purchases into savings

- Saving tax refunds

- Depositing bonuses instead of spending them

- Saving birthday or holiday cash gifts

- Reducing one unnecessary expense each week

Small actions repeated consistently often produce impressive results over time.

Avoid High-Interest Debt

Debt isn’t always bad, but high-interest debt can quickly become one of the biggest obstacles to financial success.

Understanding the difference between helpful debt and harmful debt is essential.

Good Debt vs. Bad Debt

Good Debt

Good debt is generally used to purchase something that has long-term value or helps increase future income.

Examples include:

- Student loans for valuable education

- Reasonable mortgages

- Business loans

- Certain investment loans used responsibly

Bad Debt

Bad debt usually finances items that lose value quickly or are purchased impulsively.

Examples include:

- High-interest credit cards

- Payday loans

- Buy-now-pay-later debt used irresponsibly

- Unnecessary personal loans

- Financing luxury purchases you can’t comfortably afford

The goal isn’t necessarily to avoid all debt—it’s to avoid debt that limits your financial progress.

Reduce Credit Card Balances

Credit cards can be useful financial tools when paid in full each month.

Problems arise when balances remain unpaid and interest begins to accumulate.

Helpful strategies include:

- Pay more than the minimum payment.

- Avoid making new unnecessary purchases.

- Focus extra payments on the highest-interest debt first.

- Continue making minimum payments on all other debts.

This approach often saves money on interest over time.

Create a Debt Repayment Plan

Two popular repayment strategies are:

Debt Snowball

- Pay off the smallest balance first.

- Gain motivation from quick wins.

- Move to the next smallest debt.

Debt Avalanche

- Pay off the highest interest rate first.

- Save more money on interest.

- Often results in faster long-term repayment.

Choose the strategy that best matches your personality and financial situation. The most effective plan is the one you consistently follow.

Set Clear Financial Goals

Financial goals provide direction for every budgeting and saving decision.

Without goals, it’s easy to spend money on short-term wants instead of long-term priorities.

Well-defined goals help you stay motivated and measure your progress.

Short-Term Goals

Goals achievable within one year may include:

- Build a $1,000 emergency fund

- Pay off a credit card

- Save for a vacation

- Purchase a laptop

- Start investing

These goals create momentum and confidence.

Medium-Term Goals

These generally take one to five years.

Examples include:

- Buy a reliable vehicle

- Save for a home down payment

- Launch a small business

- Complete professional training

- Reach a savings milestone

Medium-term goals often require disciplined budgeting and consistent monthly contributions.

Long-Term Goals

Long-term financial goals typically extend beyond five years.

Examples include:

- Financial independence

- Retirement savings

- Paying off a mortgage

- Funding children’s education

- Building investment income

- Creating generational wealth

Long-term goals become much more achievable when broken into smaller monthly targets.

Use SMART Goals

A strong financial goal should be:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Instead of saying:

“I want to save more money.”

Say:

“I will save $5,000 within the next 12 months by setting aside $417 each month.”

Specific goals are easier to track and accomplish.

Learn Basic Investing

Saving protects your money, but investing gives it the opportunity to grow.

Inflation gradually reduces purchasing power, meaning money kept only in a regular savings account may lose value over time.

Investing helps your money work for you.

Why Investing Matters

Investments have the potential to generate returns through:

- Capital appreciation

- Dividends

- Interest

- Compound growth

The earlier you begin investing, the more time your investments have to grow.

For many people, time is the most valuable investing advantage.

Beginner Investment Options

Beginners should focus on understanding investments before chasing high returns.

Common investment options include:

Index Funds

Index funds provide diversification by tracking a broad market index.

Benefits include:

- Lower fees

- Long-term growth potential

- Reduced risk compared to individual stocks

Exchange-Traded Funds (ETFs)

ETFs combine diversification with flexibility and are often suitable for beginner investors.

Advantages include:

- Easy to buy and sell

- Broad market exposure

- Lower costs

Retirement Accounts

If retirement accounts offer tax advantages in your country, contributing regularly can significantly increase long-term wealth.

Even modest monthly contributions may grow substantially over several decades.

Individual Stocks

While individual stocks can provide strong returns, they also involve greater risk.

Beginners should research thoroughly and avoid investing money they cannot afford to leave invested for the long term.

Understand Compound Growth

Compound growth is one of the most powerful concepts in personal finance.

When your investment earns returns, and those returns also begin earning returns, your wealth can grow at an accelerating rate.

Example:

Investing $200 each month consistently over many years may result in significantly more wealth than waiting several years to start—even if the monthly contribution stays the same.

This illustrates why starting early often matters more than investing large amounts later.

Invest Consistently

Successful investors rarely try to predict short-term market movements.

Instead, they:

- Invest regularly.

- Stay diversified.

- Think long term.

- Avoid emotional decisions.

- Continue learning.

Consistency is usually more important than trying to perfectly time the market.

Building wealth through investing is a marathon, not a sprint. Patience, discipline, and continuous learning are the habits that separate successful long-term investors from those who chase quick profits.

Improve Financial Literacy

Financial literacy is the ability to understand and confidently use financial knowledge in everyday life. It includes budgeting, saving, borrowing, investing, taxes, insurance, and retirement planning. The more financially literate you become, the easier it is to make informed decisions that support your long-term goals.

One of the best investments you can make is investing in your own financial education. Unlike market trends or economic conditions, knowledge stays with you and continues to provide value throughout your life.

Read Personal Finance Books

Books remain one of the most reliable ways to build a strong financial foundation. Reading from respected financial experts exposes you to proven principles that have helped millions of people improve their money management skills.

Aim to read at least one personal finance book every few months. Take notes, apply the lessons, and revisit the concepts as your financial situation changes.

Follow Trusted Financial Resources

The internet offers an abundance of financial information, but not all of it is accurate or trustworthy. Follow reputable financial educators, government agencies, educational institutions, and established financial publications.

When researching financial advice, always ask:

- Is the information supported by credible sources?

- Does it encourage responsible financial behavior?

- Is it focused on long-term success rather than quick riches?

Avoid influencers or websites that promise guaranteed profits, unrealistic investment returns, or “secret” methods for getting rich quickly.

Continue Learning

Personal finance is an ongoing journey. New financial tools, investment opportunities, tax rules, and technologies continue to evolve.

Set aside time each month to:

- Read finance articles

- Listen to educational podcasts

- Watch expert interviews

- Attend webinars

- Learn about budgeting apps and financial tools

Small, consistent learning habits can significantly improve your financial decision-making over time.

Develop Healthy Spending Habits

Building wealth isn’t only about earning more—it’s also about spending wisely. Healthy spending habits help you align your purchases with your priorities while avoiding unnecessary financial stress.

Know the Difference Between Needs and Wants

One of the simplest ways to improve your finances is to separate essential expenses from discretionary spending.

Needs

These are expenses required for daily living, including:

- Housing

- Utilities

- Groceries

- Transportation

- Healthcare

- Insurance

- Essential clothing

Wants

These are purchases that improve your lifestyle but are not essential, such as:

- Dining out

- Premium subscriptions

- Luxury clothing

- Entertainment

- Travel upgrades

- The latest gadgets

Understanding this difference helps you make intentional spending decisions without feeling deprived.

Practice Mindful Spending

Before making a purchase, ask yourself:

- Do I really need this?

- Will I still value this purchase a month from now?

- Does it support my financial goals?

- Can I comfortably afford it?

This simple habit can reduce impulse buying and help you focus on purchases that genuinely improve your quality of life.

Follow the 24-Hour Rule

For non-essential purchases, wait at least 24 hours before buying.

This pause gives you time to evaluate whether the purchase is truly necessary or simply an emotional decision.

Many people discover they no longer want the item after waiting a day, helping them save money without feeling restricted.

Avoid Lifestyle Inflation

As your income grows, it’s tempting to increase your spending just as quickly. This is known as lifestyle inflation.

Instead of spending every raise or bonus, consider:

- Increasing retirement contributions

- Growing your emergency fund

- Paying down debt

- Investing more

- Saving for future goals

Allow your savings rate to grow alongside your income.

Protect Your Financial Future

Good financial habits include preparing for risks as well as opportunities. Protecting your finances today can prevent major setbacks tomorrow.

Build Financial Security with Insurance

Insurance helps reduce the financial impact of unexpected events.

Depending on your circumstances, you may need:

- Health insurance

- Home or renters insurance

- Auto insurance

- Life insurance

- Disability insurance

Review your coverage regularly to ensure it still meets your needs.

Plan for Retirement Early

Retirement may seem far away, but starting early gives your investments more time to benefit from compound growth.

Even modest monthly contributions can grow significantly over several decades.

The earlier you begin, the less you may need to contribute each month to reach your retirement goals.

Review Your Finances Regularly

Schedule a monthly financial checkup.

Review:

- Income

- Spending

- Savings progress

- Investments

- Debt balances

- Upcoming expenses

- Financial goals

A monthly review helps you identify problems early and celebrate progress, keeping you motivated throughout your financial journey.

Practical Tips to Build Better Financial Habits

Improving your finances doesn’t require dramatic changes. Small actions performed consistently often produce the greatest long-term results.

Here are practical strategies you can begin using today:

- Track every expense for at least 30 days.

- Create a realistic monthly budget.

- Save before spending.

- Build an emergency fund.

- Automate your savings.

- Review subscriptions every three months.

- Cook more meals at home.

- Compare prices before making large purchases.

- Pay credit card balances on time.

- Set monthly savings goals.

- Invest consistently, even if you start with a small amount.

- Avoid emotional shopping.

- Learn one new financial concept each week.

- Review your financial progress every month.

- Celebrate milestones to stay motivated.

Consistency matters more than perfection.

Common Financial Mistakes Beginners Should Avoid

Everyone makes financial mistakes from time to time, but avoiding common pitfalls can save you years of stress and thousands of dollars.

Living Without a Budget

Without a budget, it’s easy to overspend and lose track of where your money goes.

Ignoring Emergency Savings

Unexpected expenses are inevitable. An emergency fund helps you avoid relying on expensive debt during difficult times.

Carrying High-Interest Credit Card Debt

Paying only the minimum balance can result in significant interest charges over time.

Delaying Investing

Waiting years to begin investing means missing valuable opportunities for compound growth.

Spending More After Every Raise

Lifestyle inflation can prevent higher income from improving your overall financial health.

Making Emotional Purchases

Buying items to relieve stress or boredom often leads to buyer’s remorse and unnecessary spending.

Not Setting Financial Goals

Without clear goals, it’s difficult to stay motivated or measure progress.

Ignoring Financial Education

The financial world constantly changes. Continuing to learn helps you make better decisions throughout your life.

Expert Tips for Long-Term Financial Success

Successful money management isn’t about finding shortcuts—it’s about following timeless principles consistently.

Keep these expert tips in mind:

- Spend less than you earn.

- Save automatically every payday.

- Invest regularly for the long term.

- Avoid unnecessary debt.

- Build multiple income streams when possible.

- Increase your savings rate after every salary increase.

- Review your financial goals every six months.

- Keep learning about personal finance.

- Focus on steady progress instead of quick results.

- Remember that consistency beats perfection.

Financial success is rarely built through one big decision. Instead, it’s the result of hundreds of smart choices made over many years.

Key Takeaways

- Smart financial habits are built through consistency, not perfection.

- Tracking your income and expenses gives you greater financial awareness.

- A realistic budget helps you control spending and prioritize savings.

- Paying yourself first makes saving automatic and sustainable.

- An emergency fund protects you from unexpected expenses.

- Avoiding high-interest debt keeps more money working toward your goals.

- Clear financial goals provide motivation and direction.

- Investing early allows compound growth to work in your favor.

- Financial education is a lifelong investment with lasting benefits.

- Small daily improvements can lead to significant long-term financial success.

By applying these principles consistently, you’ll create a stronger financial foundation and move closer to achieving lasting financial freedom.

Frequently Asked Questions (FAQs)

1. What are smart financial habits?

Smart financial habits are consistent money management practices that help you control spending, save regularly, avoid unnecessary debt, invest wisely, and achieve long-term financial goals. These habits improve financial stability and reduce money-related stress.

2. Why are financial habits important for beginners?

Beginners who develop good financial habits early are more likely to avoid debt, build emergency savings, make informed financial decisions, and create long-term wealth. Small habits practiced consistently often have a greater impact than occasional large financial decisions.

3. How much of my income should I save each month?

A common recommendation is to save at least 20% of your income whenever possible. However, if that’s not realistic, start with any amount you can afford—even 5% or 10%—and gradually increase your savings over time.

4. What is the 50/30/20 budgeting rule?

The 50/30/20 rule divides your after-tax income into three categories:

- 50% for essential needs

- 30% for personal wants

- 20% for savings, investing, and debt repayment

This budgeting method is simple, flexible, and beginner-friendly.

5. How much should I keep in an emergency fund?

Start with a goal of saving $500 to $1,000 for unexpected expenses. Once you’ve reached that milestone, aim to build an emergency fund that covers three to six months of essential living expenses.

6. Should beginners start investing immediately?

Yes. If your finances allow, beginning to invest early gives your money more time to benefit from compound growth. Even small, regular investments can grow significantly over the long term.

7. What’s the biggest financial mistake beginners make?

One of the most common mistakes is spending without a budget. Other frequent mistakes include ignoring emergency savings, carrying high-interest debt, delaying investing, and making impulse purchases without considering long-term goals.

8. How can I improve my financial habits?

You can improve your financial habits by tracking your expenses, creating a monthly budget, saving automatically, reducing unnecessary spending, setting financial goals, continuing your financial education, and reviewing your finances regularly.

9. How often should I review my budget?

Review your budget at least once a month. Monthly reviews help you identify spending patterns, adjust for changes in income or expenses, and stay on track with your financial goals.

10. Can small financial habits really make a difference?

Absolutely. Saving a small amount consistently, avoiding unnecessary purchases, and investing regularly may seem minor at first, but these habits compound over time and can lead to significant financial growth.

Featured Snippet Answer

What Are Smart Financial Habits?

Smart financial habits are daily or monthly money management practices that help individuals budget effectively, save consistently, avoid unnecessary debt, invest wisely, and plan for future financial goals. Developing these habits early can improve financial stability, reduce stress, and build long-term wealth.

People Also Ask

- How do beginners start managing money?

- What is the best budgeting method for beginners?

- How much money should I save each month?

- What financial habits build wealth?

- Why is an emergency fund important?

- How do I stop impulse spending?

- What are the biggest money mistakes young adults make?

- When should I start investing?

- How can I become financially disciplined?

- What are the keys to financial freedom?

Voice Search Optimization

Q: What are the best financial habits for beginners?

A: The best financial habits include creating a monthly budget, tracking expenses, saving before spending, building an emergency fund, avoiding high-interest debt, investing regularly, and continuously improving your financial knowledge.

Final Conclusion

Building wealth doesn’t happen overnight, and there are no shortcuts to lasting financial success. The good news is that you don’t need a high income or advanced financial knowledge to improve your financial future. What truly matters is developing smart financial habits and practicing them consistently.

Start by understanding where your money goes, create a realistic budget, save before you spend, and set achievable financial goals. Over time, these small actions become routines that strengthen your financial confidence and help you make better decisions.

Remember that progress is more important than perfection. Even if you begin with small savings or minor adjustments to your spending habits, every positive step brings you closer to financial stability and long-term wealth.

Financial freedom isn’t built through luck—it’s built through discipline, patience, and continuous learning. The habits you develop today can shape the opportunities you enjoy tomorrow.

Are you ready to take control of your finances?

Start with just one smart financial habit today—whether it’s creating your first budget, tracking your daily expenses, or opening a dedicated savings account. Small actions, repeated consistently, can transform your financial future.

If you found this guide helpful, share it with friends and family, bookmark it for future reference, and explore more personal finance and productivity resources on ProDPS.com to continue your journey toward financial confidence and long-term success.