The Wealth-Building Habits Rich People Practice Every Month: 15 Smart Financial Habits That Build Lasting Wealth

WhatsApp

Telegram

Facebook

Twitter

LinkedIn

Join Our WhatsApp Channel

Why Monthly Financial Habits Matter

Many people think building wealth is all about earning more money. While increasing your income certainly helps, it’s only one part of the equation. The real difference between long-term financial success and constant financial stress often comes down to the habits you practice consistently.

Monthly financial habits give you a regular opportunity to evaluate your progress, adjust your plans, and stay focused on your goals. Instead of waiting until the end of the year to review your finances, a monthly routine helps you identify problems before they become expensive mistakes.

Think of your finances like maintaining a healthy garden. Watering the plants once a year won’t produce good results. Small, consistent actions every month—saving, investing, budgeting, and reviewing your progress—allow your wealth to grow steadily over time.

Another advantage of monthly habits is that they reduce emotional decision-making. When you have a structured routine, you’re less likely to make impulsive purchases, panic during market downturns, or forget important financial responsibilities.

Benefits of Monthly Financial Reviews

- Stay aware of your spending habits.

- Catch budgeting problems early.

- Increase savings consistency.

- Build confidence in managing money.

- Improve investment decisions.

- Reduce financial stress.

- Make measurable progress toward long-term goals.

Habit #1: Review Your Income and Expenses Every Month

Why It Matters

One of the simplest but most powerful wealth-building habits is reviewing where your money comes from and where it goes.

Many people know roughly how much they earn but have only a vague idea of where their money disappears each month. Small recurring expenses—unused subscriptions, frequent food delivery, impulse shopping, or convenience purchases—can quietly consume hundreds of dollars over the course of a year.

A monthly income and expense review helps you spot these patterns and make informed decisions.

What to Review

Take 20–30 minutes at the end of each month to answer questions like:

- How much income did I receive?

- Which income sources increased?

- Which expenses were necessary?

- Which expenses were avoidable?

- Did I stay within my budget?

- How much did I save?

- How much did I invest?

- What surprised me this month?

Practical Example

Imagine Sarah earns $4,500 each month. During her monthly review, she discovers she’s spending:

- $120 on streaming subscriptions

- $240 on takeout meals

- $90 on impulse online shopping

That’s $450 every month, or $5,400 per year.

Instead of eliminating everything, she reduces those expenses by half and automatically invests the savings. Over several years, those consistent investments have the potential to grow through compound returns, illustrating how small monthly changes can lead to meaningful long-term results.

Easy Ways to Track Expenses

You don’t need expensive software.

Simple options include:

- A spreadsheet

- A budgeting app

- Your online banking dashboard

- Monthly credit card statements

- A personal finance notebook

The best system is the one you’ll actually use consistently.

Habit #2: Update Your Monthly Budget

A Budget Is a Living Plan

Many people create a budget once and never look at it again.

Successful wealth builders understand that budgets should change as life changes.

Income increases.

Unexpected bills happen.

Family needs change.

Inflation affects prices.

Financial goals evolve.

Updating your budget every month keeps it realistic rather than restrictive.

Focus on Priorities

When reviewing your budget, ask yourself:

Essential Expenses

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Healthcare

Financial Priorities

- Emergency savings

- Retirement contributions

- Investments

- Debt payments

Lifestyle Spending

- Dining out

- Entertainment

- Shopping

- Hobbies

- Travel

This exercise helps ensure your spending reflects your values instead of short-term impulses.

Try the 50/30/20 Rule

If you’re new to budgeting, consider using the popular 50/30/20 framework as a starting point:

| Category | Suggested Percentage |

|---|---|

| Needs | 50% |

| Wants | 30% |

| Savings & Investments | 20% |

This isn’t a strict rule but a helpful guideline. Depending on your circumstances, you may choose to save or invest a higher percentage as your income grows.

Monthly Budget Checklist

Before each new month:

- Review last month’s spending.

- Adjust for upcoming expenses.

- Plan for birthdays, holidays, or travel.

- Increase savings if possible.

- Eliminate unnecessary recurring costs.

- Set a spending limit for discretionary purchases.

Habit #3: Set Clear Financial Goals for the Month

Why Monthly Goals Work

Large financial goals can feel overwhelming.

Goals like buying a home, retiring early, or building a six-figure investment portfolio often take years to achieve. Breaking them into smaller monthly milestones makes them easier to manage and track.

Monthly goals also create accountability. Rather than saying, “I want to save more,” you can define a specific target and measure your progress.

Examples of monthly financial goals include:

- Save $300 toward an emergency fund.

- Invest $200 in a diversified portfolio.

- Pay an extra $100 toward high-interest debt.

- Read one personal finance book.

- Cancel one subscription you no longer use.

Use the SMART Framework

A helpful way to set financial goals is to make them:

- Specific: Clearly define the objective.

- Measurable: Use numbers you can track.

- Achievable: Keep goals realistic for your budget.

- Relevant: Align goals with your long-term priorities.

- Time-bound: Set a monthly deadline.

For example, instead of saying “I’ll spend less,” try “I’ll reduce dining-out expenses by $75 this month and transfer the savings into my investment account.”

Review and Celebrate Progress

At the end of each month, compare your results with your goals. Even if you don’t achieve every target, reviewing what worked and what didn’t helps you improve over time.

Celebrate small wins, such as reaching a savings milestone or sticking to your budget for the entire month. Positive reinforcement can make it easier to maintain good financial habits over the long term.

Quick Action Checklist

Before the next month begins, complete these tasks:

- ✔ Review every source of income.

- ✔ Categorize all expenses.

- ✔ Identify one unnecessary expense to reduce.

- ✔ Update your monthly budget.

- ✔ Plan for upcoming bills and events.

- ✔ Set three realistic financial goals.

- ✔ Schedule your next monthly money review on your calendar.

Main Content (Continued)

Habit #4: Pay Yourself First

What Does “Pay Yourself First” Mean?

One of the most common habits among financially successful people is treating savings and investing like a mandatory monthly bill.

Instead of saving whatever money happens to be left at the end of the month, they move a predetermined amount into savings or investments immediately after receiving their income.

This strategy helps ensure that wealth-building remains a priority rather than an afterthought.

Why This Habit Works

When savings depend on leftover money, there often isn’t much left. Monthly expenses, unexpected purchases, and impulse spending can quickly consume your income.

By paying yourself first, you’re making a commitment to your future before spending on discretionary items.

Benefits

- Builds savings consistently.

- Reduces the temptation to overspend.

- Creates long-term financial discipline.

- Supports investment growth through consistency.

- Makes achieving financial goals more predictable.

Automate the Process

Automation removes the need for willpower.

Consider setting up automatic transfers for:

- Emergency fund contributions

- Retirement savings

- Investment accounts

- Children’s education savings

- Debt repayment above the minimum payment

Even small automatic contributions can make a significant difference over time.

Example

Suppose James automatically invests $300 every month.

He never has to remember to make the transfer.

Because the money leaves his account immediately after payday, he naturally adjusts his spending to what’s available instead of trying to save what’s left over.

This simple system reduces financial stress and encourages long-term consistency.

Habit #5: Invest Consistently Every Month

Consistency Beats Perfect Timing

Many new investors wait for the “perfect” time to invest.

In reality, predicting short-term market movements consistently is extremely difficult.

Long-term investors often focus on investing regularly rather than trying to buy only at the lowest prices.

One widely used approach is dollar-cost averaging, where you invest a fixed amount at regular intervals regardless of market conditions. This can reduce the impact of short-term price fluctuations over time.

Why Monthly Investing Matters

Regular investing offers several potential benefits:

- Encourages long-term discipline.

- Removes emotional decision-making.

- Helps build wealth gradually.

- Allows compound growth to work over time.

- Fits easily into a monthly budget.

Diversification Is Important

Rather than relying on a single investment, many investors spread their money across different asset types to reduce risk.

Depending on your goals and risk tolerance, a diversified portfolio may include:

- Broad-market stock funds

- Bond funds

- International investments

- Real estate investments

- Cash or cash equivalents

Diversification cannot eliminate investment risk, but it can help reduce the impact of poor performance from any single investment.

Start Small

You don’t need a large amount of money to begin investing.

Many investment platforms allow people to start with relatively small monthly contributions.

The important part is building the habit—not waiting until you believe you have “enough” money.

Habit #6: Review Your Investment Portfolio

Why Monthly Reviews Matter

Reviewing your portfolio doesn’t mean making constant changes.

Instead, it’s an opportunity to confirm that your investments still align with your financial goals, time horizon, and risk tolerance.

Monthly reviews can help you:

- Track performance.

- Monitor diversification.

- Check contribution progress.

- Identify major changes.

- Stay focused on long-term objectives.

Avoid reacting emotionally to normal market fluctuations. Investing is generally a long-term process, and short-term volatility is common.

Questions to Ask During Your Review

- Am I still investing consistently?

- Has my asset allocation changed significantly?

- Am I taking more risk than intended?

- Have my financial goals changed?

- Should I increase my monthly investment amount?

The goal is thoughtful evaluation—not frequent buying and selling.

Habit #7: Track Your Net Worth

What Is Net Worth?

Your net worth is one of the clearest indicators of your overall financial progress.

It’s calculated by subtracting your liabilities from your assets.

Formula

Net Worth = Total Assets − Total Liabilities

Assets May Include

- Savings accounts

- Investment accounts

- Retirement accounts

- Real estate

- Business interests

- Vehicles (where appropriate)

Liabilities May Include

- Credit card balances

- Student loans

- Personal loans

- Auto loans

- Mortgage balances

Why Track It Monthly?

Income alone doesn’t tell the whole story.

A person with a high salary but significant debt may have a lower net worth than someone earning less but consistently saving and investing.

Tracking your net worth each month helps you see whether your financial decisions are moving you in the right direction.

Even modest monthly improvements can add up significantly over the years.

Practical Monthly Wealth-Building Checklist

Use this checklist at the end of every month to stay on track.

| Task | Complete |

|---|---|

| Review monthly income | ☐ |

| Review monthly expenses | ☐ |

| Update budget | ☐ |

| Transfer money to savings | ☐ |

| Invest monthly | ☐ |

| Review investment portfolio | ☐ |

| Track net worth | ☐ |

| Pay down high-interest debt | ☐ |

| Review financial goals | ☐ |

| Plan next month’s priorities | ☐ |

Consider printing this checklist or saving it digitally so you can revisit it every month.

Real-Life Example: Small Habits, Big Results

Imagine two friends, Alex and Taylor, both earning similar incomes.

Alex waits until the end of each month to save whatever is left. Some months it’s $50, other months it’s nothing.

Taylor follows a monthly financial routine:

- Reviews spending.

- Updates a budget.

- Automatically saves 15% of income.

- Invests a fixed amount each month.

- Tracks net worth.

- Reviews long-term goals.

After several years, Taylor is likely to have accumulated more savings and investments—not because of earning dramatically more, but because of consistently following a structured financial plan.

This example illustrates an important principle: sustainable wealth often grows from disciplined habits repeated over time rather than one-time financial decisions.

Monthly Success Checklist

Before the month ends, ask yourself:

- Did I spend intentionally?

- Did I save before spending?

- Did I invest this month?

- Did I reduce unnecessary expenses?

- Did I make progress toward my financial goals?

- Did I learn something new about personal finance?

- What one habit can I improve next month?

Thanks! Below is Part 3A of your publication-ready blog post.

Habit #8: Build and Protect an Emergency Fund

Why an Emergency Fund Is Essential

Unexpected expenses are a part of life. A medical bill, car repair, job loss, or urgent home maintenance can disrupt even the best financial plan. Without an emergency fund, many people rely on credit cards or loans, which can lead to long-term debt.

An emergency fund acts as a financial safety net. It allows you to handle unexpected costs without sacrificing your long-term goals or investments.

How Much Should You Save?

The ideal amount depends on your personal situation, but a common guideline is to save enough to cover three to six months of essential living expenses.

If you’re self-employed or have an irregular income, you may choose to build a larger emergency fund for additional security.

Tips for Growing Your Emergency Fund

- Set a monthly savings target.

- Keep the money in a separate savings account.

- Avoid using it for non-emergency purchases.

- Replenish the fund after using it.

- Increase contributions when your income grows.

Remember, building an emergency fund takes time. Even starting with a small monthly contribution is better than waiting for the “perfect” moment.

Habit #9: Eliminate High-Interest Debt

Why Debt Can Slow Wealth Building

Not all debt is the same. While some loans may support long-term goals, high-interest debt—such as credit card balances—can significantly reduce your ability to save and invest.

Every dollar spent on interest is a dollar that cannot be used to grow your wealth.

Reducing high-interest debt should be one of your monthly financial priorities.

Debt Repayment Strategies

The Avalanche Method

Focus on paying off the debt with the highest interest rate first while making minimum payments on other balances.

Best for: Reducing total interest paid over time.

The Snowball Method

Pay off the smallest balance first, then move to the next one after each debt is cleared.

Best for: Staying motivated through quick wins.

Neither method is universally better. The right choice depends on your financial situation and what helps you stay consistent.

Monthly Debt Review Checklist

- Check outstanding balances.

- Make all payments on time.

- Pay more than the minimum whenever possible.

- Avoid adding unnecessary new debt.

- Track your progress each month.

Habit #10: Create Multiple Income Streams

Why Diversifying Income Matters

Relying on a single source of income can increase financial risk. If that income stops unexpectedly, it may become difficult to cover everyday expenses or continue investing.

Developing additional income streams can improve financial stability and create more opportunities to save and invest.

Keep in mind that building extra income often takes time, effort, and planning.

Examples of Additional Income Streams

- Freelancing or consulting

- Selling digital products

- Affiliate marketing

- Dividend-paying investments

- Rental income

- Online courses or coaching

- Print-on-demand products

- Blogging or content creation

- YouTube or podcast monetization

- Photography or design licensing

Choose opportunities that align with your skills, interests, and available time.

Monthly Action Step

Ask yourself:

What can I do this month to increase my income by even a small amount?

Small increases can add up over time, especially when invested consistently.

Habit #11: Continue Learning About Money

Financial Education Is an Ongoing Process

Financial markets, tax rules, investment options, and technology continue to evolve. Successful wealth builders make learning a lifelong habit.

Improving your financial knowledge can help you make more informed decisions and avoid common mistakes.

Ways to Learn Every Month

- Read a personal finance book.

- Follow reputable financial educators.

- Listen to finance podcasts.

- Watch educational webinars.

- Read articles from trusted financial publications.

- Take an online course.

- Learn about investing, budgeting, or retirement planning.

Even dedicating 20–30 minutes each week can lead to meaningful improvements over time.

Be Selective About Information

Not all financial advice online is reliable.

Look for information from qualified professionals, government agencies, educational institutions, and established financial organizations. Be cautious of anyone promising guaranteed returns or “get rich quick” strategies.

Habit #12: Organize Your Financial Documents

Stay Prepared

Good organization can save time, reduce stress, and make important financial decisions easier.

Keep your financial records updated and stored securely.

Documents to Organize

- Bank account information

- Investment statements

- Tax records

- Insurance policies

- Loan documents

- Retirement account details

- Monthly budgets

- Estate planning documents (if applicable)

Digital folders with secure backups can make document management more convenient while helping protect important information.

Practical Tips to Strengthen Your Monthly Wealth-Building Routine

The best financial plans are simple enough to follow consistently. Consider these practical tips:

1. Schedule a Monthly Money Date

Set aside 30–60 minutes on the same day each month to review your finances. Treat this appointment as seriously as any work meeting.

2. Automate Good Financial Habits

Whenever possible, automate savings, investments, and bill payments. Automation helps reduce missed payments and encourages consistency.

3. Increase Savings Gradually

Each time your income increases, consider directing part of the increase toward savings or investments before expanding your lifestyle.

4. Review Your Financial Goals Regularly

Your priorities may change over time. Revisit your goals monthly to ensure your financial plan still reflects what matters most.

5. Celebrate Small Wins

Reaching milestones—such as paying off a debt or increasing your savings—deserves recognition. Celebrating progress can help reinforce positive habits.

Common Mistakes That Can Slow Wealth Building

Avoiding common mistakes can be just as valuable as adopting good habits.

1. Living Beyond Your Means

Consistently spending more than you earn makes it difficult to build long-term wealth.

2. Ignoring Small Expenses

Frequent small purchases may seem insignificant, but together they can have a meaningful impact on your budget.

3. Waiting Too Long to Invest

Delaying investing may reduce the potential benefits of long-term compound growth.

4. Chasing Quick Profits

Be cautious of investments or business opportunities that promise unusually high returns with little or no risk.

5. Not Having an Emergency Fund

Unexpected expenses can quickly disrupt your financial plan if you’re unprepared.

6. Making Emotional Financial Decisions

Fear and excitement can lead to poor financial choices. A consistent monthly routine helps you stay focused on long-term goals.

7. Forgetting to Review Progress

Without regular reviews, it’s easy to drift away from your financial objectives.

Quick Monthly Wealth Checklist

Before each month ends, ask yourself:

- ✔ Did I review my budget?

- ✔ Did I save before spending?

- ✔ Did I invest this month?

- ✔ Did I reduce unnecessary expenses?

- ✔ Did I make progress toward paying off debt?

- ✔ Did I grow my emergency fund?

- ✔ Did I learn something new about personal finance?

- ✔ Did I move closer to my long-term financial goals?

Frequently Asked Questions (FAQs)

1. What are wealth-building habits?

Wealth-building habits are consistent financial behaviors that help improve your financial health over time. Examples include budgeting, saving regularly, investing consistently, tracking your expenses, reviewing your financial goals, and continuing to learn about personal finance. While no habit guarantees wealth, practicing these behaviors consistently can support long-term financial stability.

2. How often should I review my finances?

A monthly financial review is a practical routine for most people. It allows you to check your income, spending, savings, investments, debt, and progress toward your goals without becoming overwhelmed by day-to-day fluctuations.

3. Do I need a high income to build wealth?

No. While a higher income can provide more opportunities to save and invest, long-term wealth is also influenced by how consistently you manage your money. Spending wisely, avoiding unnecessary debt, saving regularly, and investing over time can make a meaningful difference regardless of income level.

4. What is the best monthly habit for building wealth?

There isn’t a single “best” habit because personal finances vary. However, many financial experts emphasize consistently paying yourself first, investing regularly, living below your means, and reviewing your finances every month as foundational habits.

5. How much should I save every month?

The right amount depends on your income, expenses, and financial goals. A common guideline is to save at least 20% of your income if possible, but even smaller amounts can help build momentum. The key is consistency and increasing your savings rate as your income grows.

6. Should I pay off debt before investing?

It depends on the type of debt and your financial situation. High-interest debt, such as many credit card balances, is often prioritized because interest costs can grow quickly. At the same time, many people continue making at least some retirement or long-term investment contributions while paying down debt. If you’re unsure, consider seeking advice from a qualified financial professional.

7. How long does it take to build wealth?

Building wealth is usually a long-term process rather than a quick result. Factors such as your income, savings rate, investment returns, and financial decisions all influence the timeline. Consistent habits practiced over many years generally have a greater impact than short-term strategies.

8. Why is tracking net worth important?

Your net worth provides a snapshot of your overall financial health by comparing what you own with what you owe. Tracking it monthly can help you measure progress, identify trends, and stay motivated as your assets grow and liabilities decrease.

9. What is the biggest mistake people make when trying to build wealth?

One of the most common mistakes is waiting for the “perfect time” to start. Delaying savings, investing, or budgeting can mean missing valuable opportunities to build healthy financial habits. Starting small and staying consistent is often more effective than waiting for ideal circumstances.

10. Can these habits help beginners?

Absolutely. The habits discussed in this guide are designed to be practical and scalable. Whether you’re managing your first paycheck or working toward financial independence, these strategies can be adapted to your current situation and goals.

Expert Tips

If you want to improve your financial future, focus on progress rather than perfection. Consider these expert-backed practices:

Prioritize Consistency Over Perfection

Missing one month isn’t the end of your financial journey. What matters most is returning to your routine and maintaining good habits over time.

Increase Savings When Your Income Increases

When you receive a raise, bonus, or additional income, consider directing part of it toward savings or investments before increasing discretionary spending.

Review Financial Goals Quarterly

While monthly reviews help you stay on track, taking a broader look every three months can help ensure your long-term goals still match your priorities.

Keep Learning

Financial knowledge evolves. Reading books, following reputable educational resources, and staying informed about personal finance can help you make better decisions over time.

Protect Your Financial Progress

Wealth building isn’t just about growing assets—it’s also about protecting them through responsible budgeting, appropriate insurance, secure passwords, and regular account monitoring.

Key Takeaways

- Wealth is typically built through consistent habits rather than one-time actions.

- Monthly financial reviews help you stay aware of your income, expenses, savings, and investments.

- Paying yourself first encourages disciplined saving and investing.

- Consistent investing can support long-term financial growth.

- An emergency fund provides financial resilience during unexpected events.

- Reducing high-interest debt can improve your overall financial position.

- Diversifying income sources may strengthen financial stability.

- Ongoing financial education helps you make informed decisions.

- Tracking your net worth offers a clear measure of long-term progress.

- Small improvements made consistently can add up over time.

Final Conclusion

Building wealth isn’t about chasing shortcuts or relying on luck. It’s about making intentional financial decisions month after month and allowing those decisions to compound over time.

The habits covered in this guide—from reviewing your budget and investing consistently to building an emergency fund and continuing your financial education—can help create a stronger financial foundation. While everyone’s journey is different, the common thread is consistency.

Remember that financial success isn’t measured solely by income. It’s also reflected in how effectively you manage your money, prepare for the unexpected, and work toward meaningful goals.

You don’t have to implement every habit at once. Choose one or two that fit your current situation, make them part of your monthly routine, and gradually build from there. Sustainable progress often comes from small, repeatable actions rather than dramatic changes.

With patience, discipline, and a long-term perspective, today’s smart financial habits can become tomorrow’s financial security.

Ready to take control of your financial future?

Start by choosing one wealth-building habit from this guide and commit to practicing it this month. Whether it’s creating a budget, reviewing your spending, increasing your savings, or making your first investment, every positive step counts.

If you found this guide helpful:

- Share it with friends and family who want to improve their financial habits.

- Save it for your next monthly financial review.

- Explore more personal finance and productivity resources on ProDPS.com to continue building your financial knowledge and long-term success.

---Advertisement---

[adinserter block="1"]

LATEST post

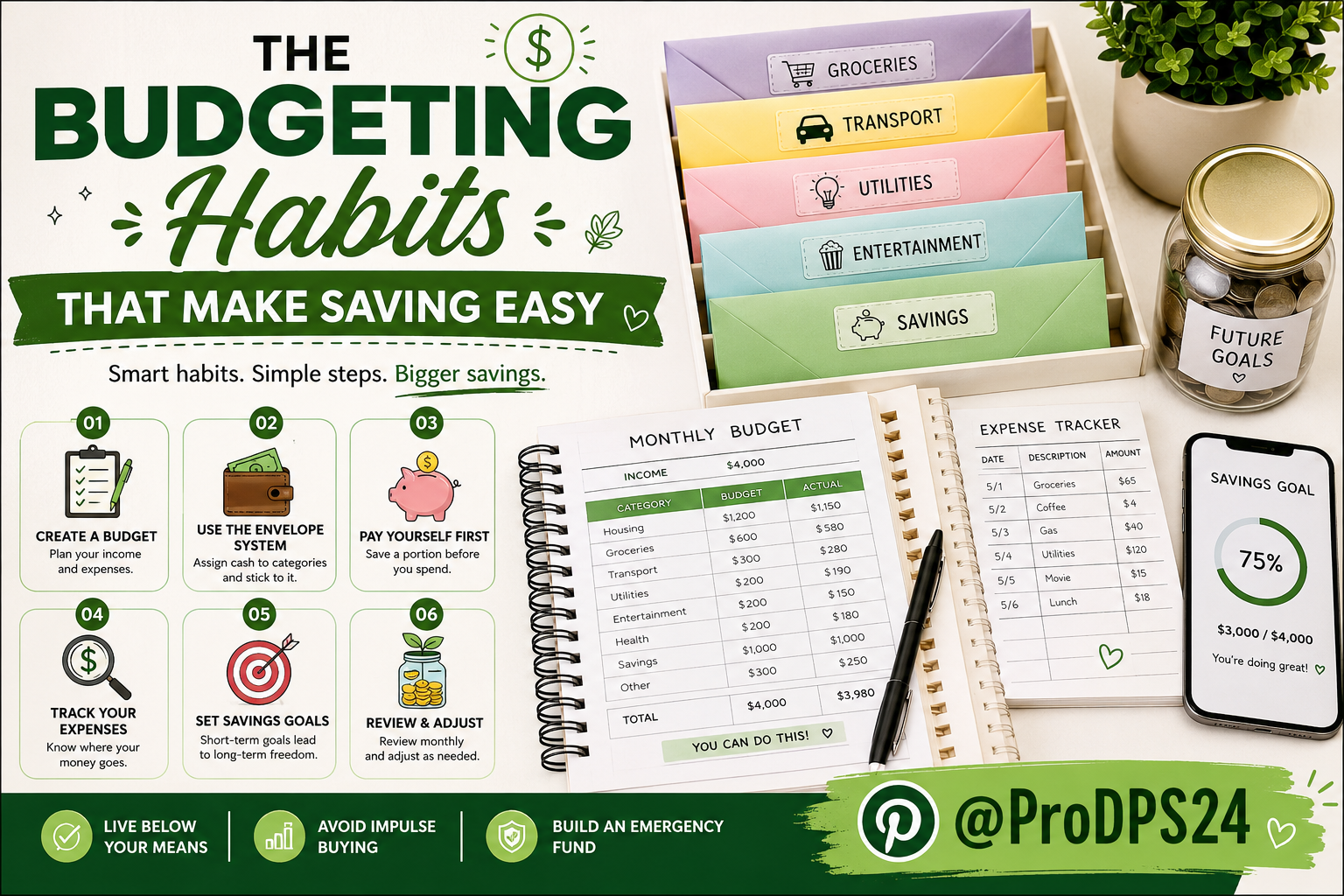

The Budgeting Habits That Make Saving Easy: 10 Simple Money Habits for Financial Success

July 11, 2026

4:03 am

20 Best Printable Products to Sell Online (High-Demand Ideas for 2026)

July 10, 2026

5:49 am

15 Best Free AI Websites You Should Bookmark in 2026

July 10, 2026

5:27 am

18 Side Hustles That Require Almost No Money (Beginner Guide)

July 9, 2026

5:08 pm

Money Mistakes That Keep People Broke (And How to Avoid Them)

July 9, 2026

4:28 pm